The financial market supervision (FMA) warns of problems with bank loans. Real estate loans remain in the sights of the supervisors. Bankers had recently criticized this.

The banks are profitable – so much that the republic re -taxed it – but the financial market supervision (FMA) sees considerable need for action. FMA board member Helmut Ettl warns of problems with bank loans.

“When the ebb comes, you can see who bathe naked. And here some were on the nudist beach. »

Helmut Ettl

FMA boss

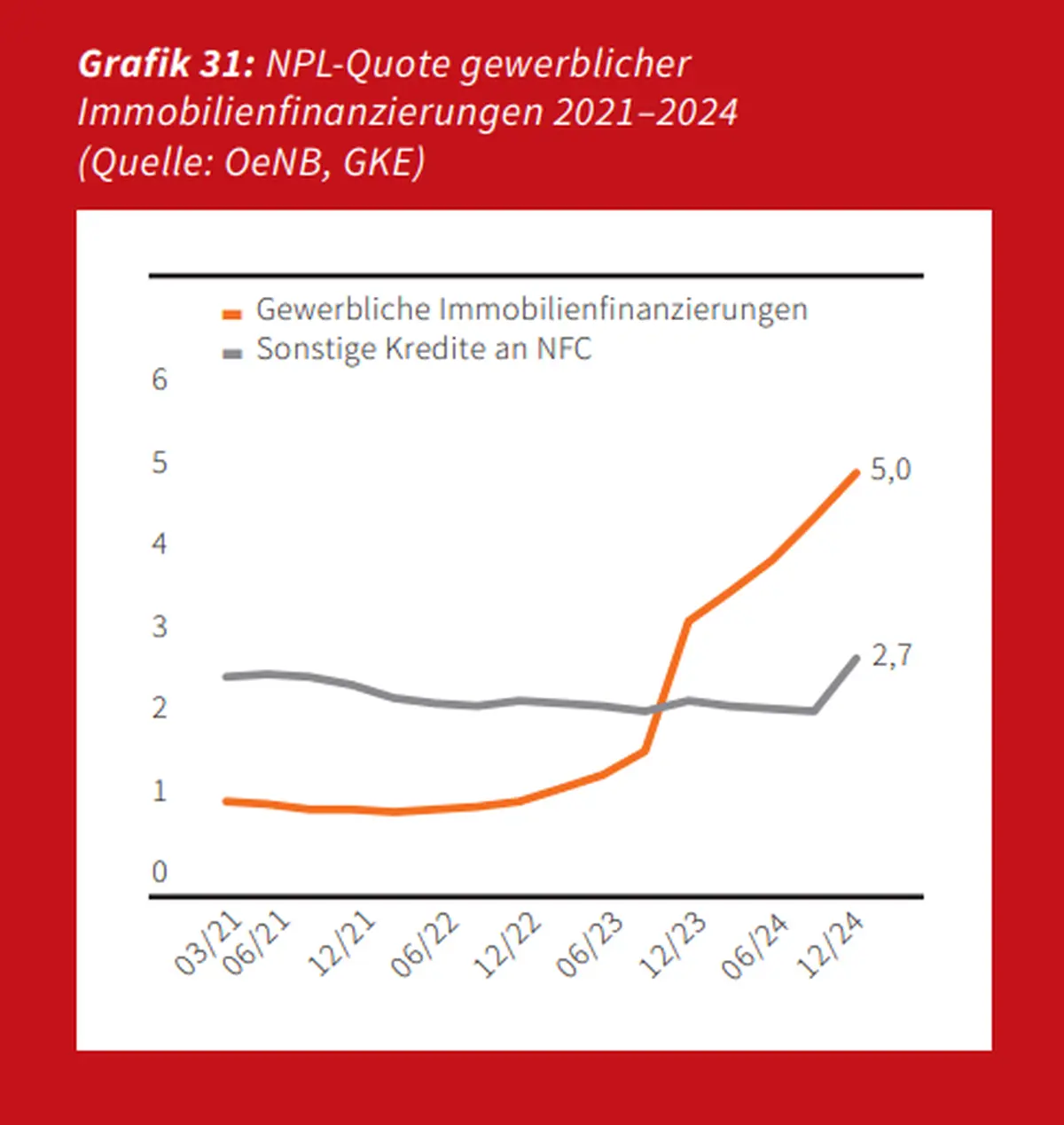

A miracle point here is the lazy loans. The proportion of necessary loans (NPL) has increased significantly and is now three percent. In 2023 it was only 2.2 percent. The main child is the sector of commercial real estate. Financing for them rose from 3.3 percent to five percent. « Not all banks are the same, some banks are very strong, » says Ettl on Thursday at the FMA’s presentation. « When the low tide comes, you can see who bathe naked. And here some were on the nudist beach. » Therefore, the supervision is targeting the sector again this year.

FMA

« />

The prices for residential properties and the income of households developed apart.FMA

Award two thirds of all real estate loans

As of July, a Sectoral buffer for the loans of commercial properties will have one percent of their portfolio. This increases the existing buffer capital by approx. € 600 million, which increases the resilience of the Austrian banking sector. You don’t know yet whether « the sole of the valley » has already been reached in the crisis, says Ettl. Therefore, the banking industry must continue to provide. Several Banker criticized Finally the measure as too exuberant. After all, it is an important business area of domestic money houses. Therefore, the focus on financial stability is so important, says Ettl. Because two thirds of all loans to households and non -financial companies make up real estate loans. At the end of 2024, the loan in private and commercial real estate loans was 263 billion euros.

FMA

« />

FMA pushes banks to further comply with the KIM regulation, although this expires in the middle of the year.FMA

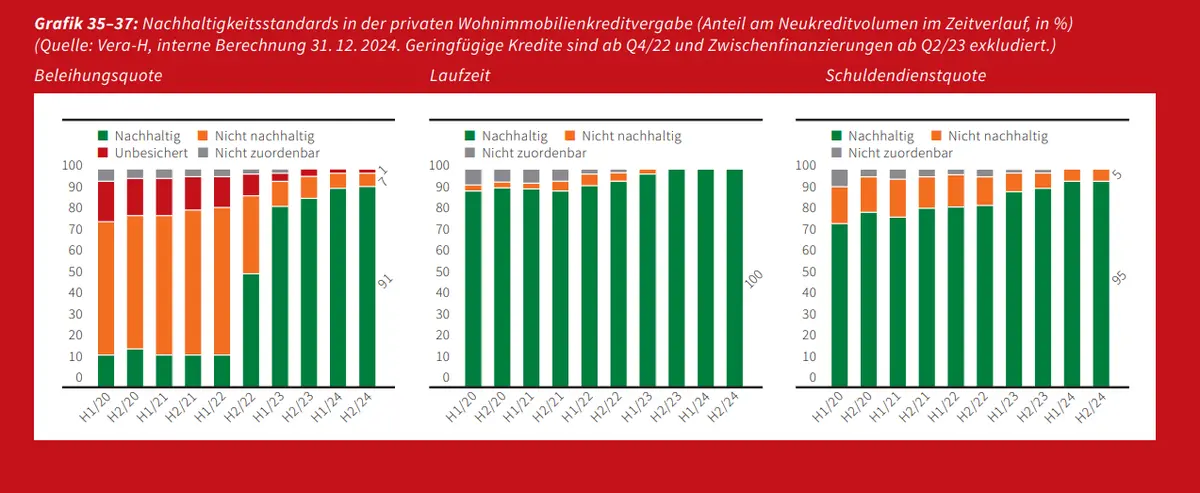

The KIM Ordinance, which enforced stricter rules in the allocation of residential property loans to private individuals, expires in the middle of the year. Nevertheless, the banks should continue to adhere to it. You should actually do that even before the KIM regulation was introduced in the summer of 2022, at least that is how the recommendation at the time. Nevertheless, you can see that lending from the second half of 2022 was much more adhered to the regulation, i.e. beforehand. Since the start of the KIM, the volume of sustainable loans (i.e. those that meet the KIM criteria) has increased by 73 percent.

FMA

« />

Lazy loans for commercial properties increased significantly.FMA

Real estate loans remain focus of the FMA

So residential property loans will probably remain in the focus of the supervision. A circular to the banks is planned here, which is reminiscent of the KIM regulations, says Ettl. « The social problems on the housing market cannot be solved through too relaxed financing. » ETTL reminds that the subprime crisis in the United States triggered people who cannot afford it to people who cannot afford it. « Housing on pump » is not a solution.

According to the « press » information, even a sectoral buffer was also planned for the financing of residential property. But the supervisors let go of it – so far.

The collapse of Signa has not only brought many other real estate companies to the bredouille, but also some bankers in need of explanation. Many “mini-signas” with adventurous constructs were created here.

Austria’s banks in the top European league

In the past year, Austria’s banks kept their profits at around 11.5 billion euros (previous year: EUR 12.6 billion) at a high level – despite significant credit provisions and individual geopolitical burdens. As in the previous year, however, the main driver for the profits was the interest income, triggered by the interest turn of the European Central Bank (ECB). With the new turning point, the residential finance will now start again, says Ettl. The quota of the hard core capital (CET-1) remained little changed to 17.5 percent and is therefore more than twice as high as before the financial crisis and, for example, on average of the euro countries. « The resilience that is currently evident has developed the finance industry bit by bit in the past 15 years, » said the FMA.

The Austrian banking system is one of the few countries in the top ranking of Standard & Poor’s risk survey, says FMA board member Eduard Müller. The Netherlands, Switzerland and the Scandinavian countries are still located in the pot field. Incidentally, it is the last record of Müller. The FMA board will be replaced by Mariana Kühnel from July.

Money laundering test in Austria in full swing

« Preparation for Austria’s fifth country examination through the Financial Action Task Force (FATF) began in 2023 and is expected to take until 2026, » says the Finance Minister Markus Marterbauer at the FMA annual financial statements. This is the review of the prevention regime of money laundering, terrorism financing and proliferation of weapons of mass destruction and significantly affects the work of the FMA in recent years.

« A positive test result is crucial for the reputation of the domestic financial center and the business location of Austria. »

Markus Marterbauer

Finance minister

« A positive test result is crucial for the reputation of the domestic financial center and the business location of Austria. » The FMA supervises 877 financial institutions, including insurers and pension funds. Last year, the supervisors made 40 on-site measures to be underwear alone. Among them z. B. at Euram Bank, which was withdrawn the license in 2024.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Toujours activé

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

reports to the police of Breda: « He eventually felt hunted » (Nijlen)")